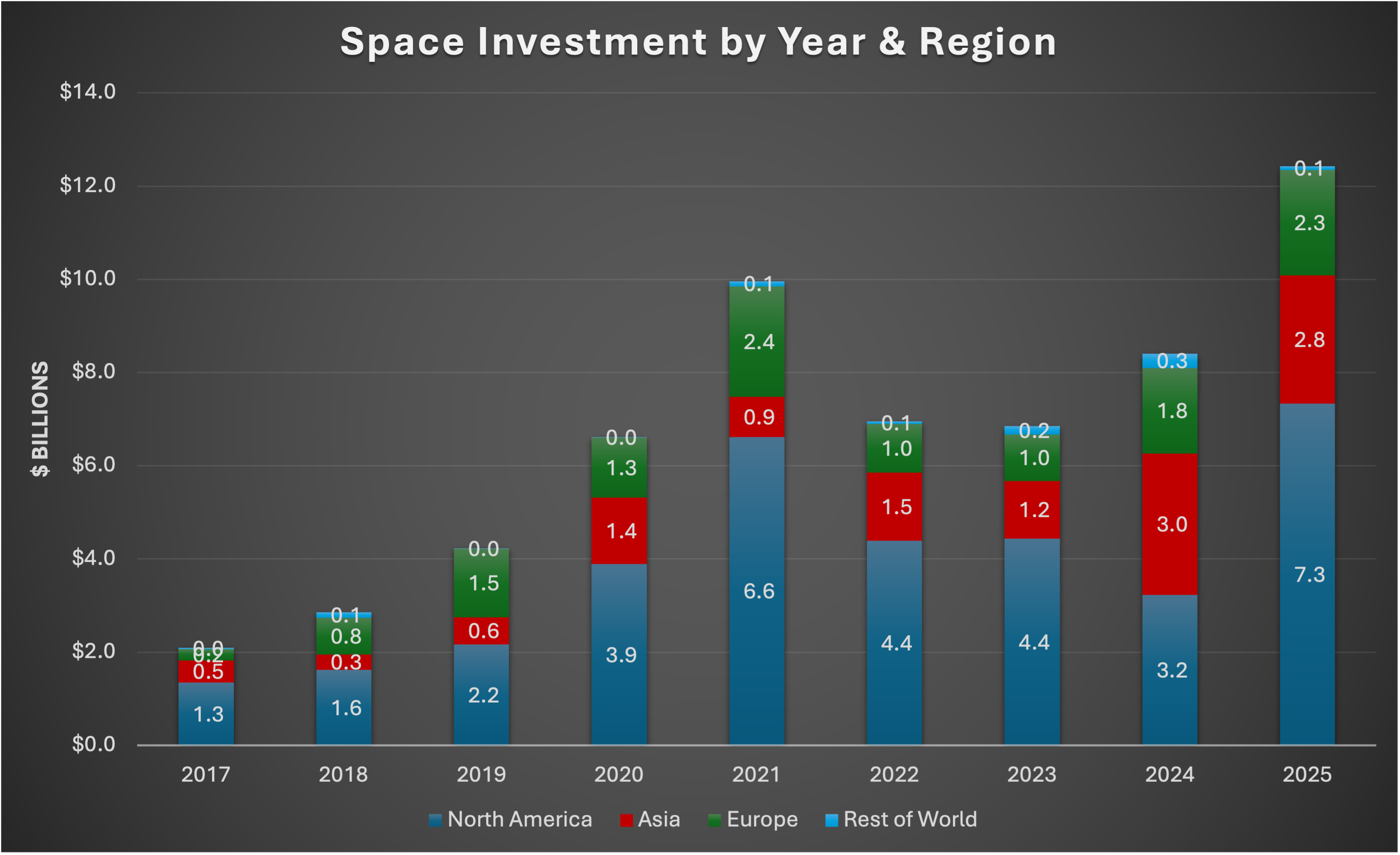

The space sector just closed its strongest year on record (see Figure 1). According to Seraphim Space's Q4 2025 investment report, private capital deployed into SpaceTech reached $12.4 billion over the trailing twelve months, surpassing the 2021 peak of $10.9 billion and significantly outperforming the broader venture capital market.

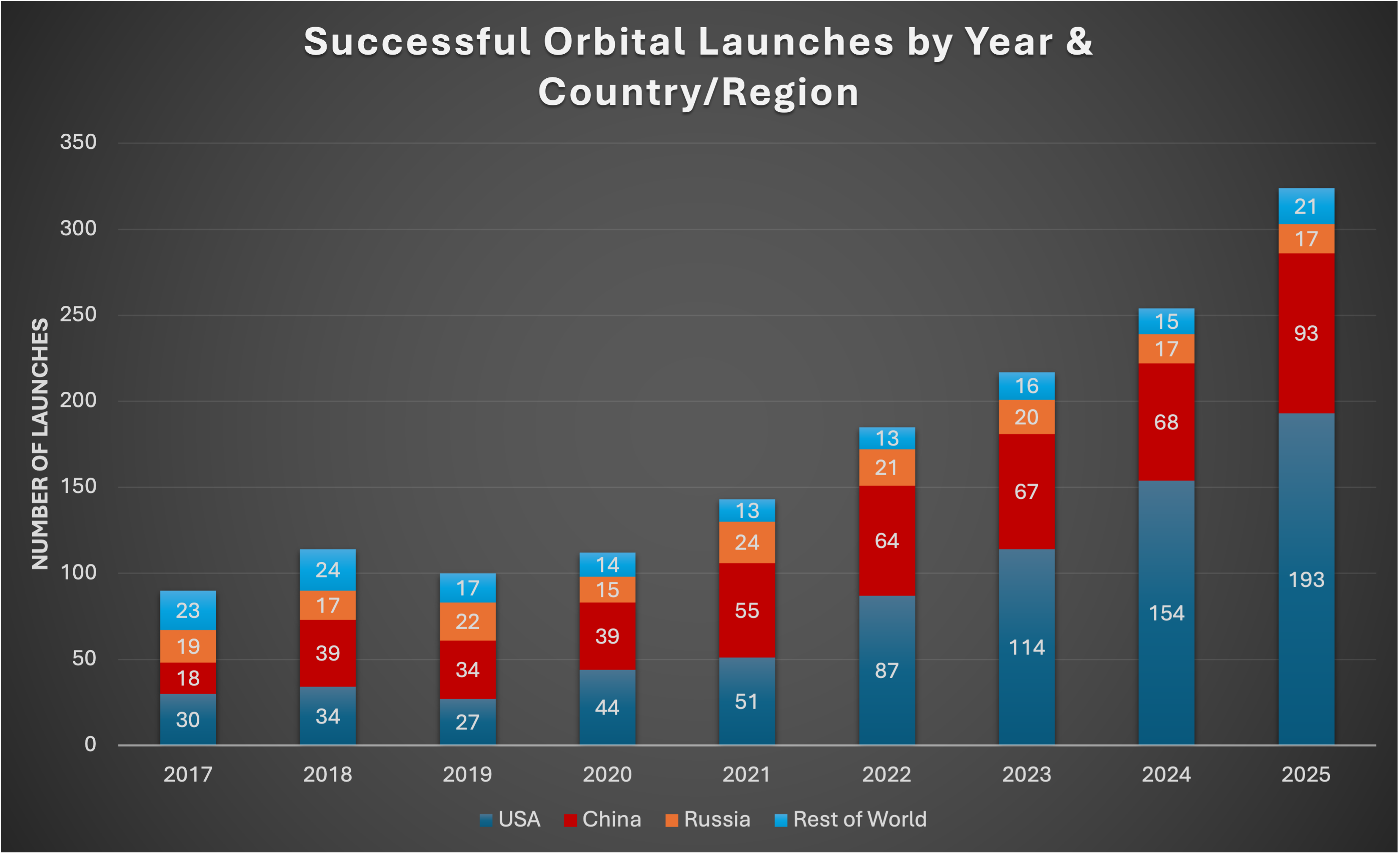

At the same, launch cadence is accelerating dramatically — and has been doing so for the last 5 years (see Figure 2). SpaceX alone flew over 130 orbital missions in 2025, while global launch activity topped 320 successful missions — nearly triple the annual rate from five years ago. Launch is no longer a constraint. It's routine infrastructure.

The consensus narrative is straightforward: launch de-risked the sector, capital is flowing back, geopolitical urgency is creating massive government demand, and commercial space markets are finally arriving at scale. After the 2022 pullback, the industry has not just recovered; it has also structurally matured.

But there’s a more consequential reading of these same numbers: one that recognizes that, rather than taking a victory lap, the sector faces a set of high-stakes choices that will determine how our future in space evolves.

The investment surge, the geopolitical tailwinds, and the flagship programs driving 2025's record capital deployment may be creating precisely the conditions that entrench mission-dependence rather than enable market formation — and doing so at a scale we've never seen before.

If that interpretation holds, this is not yet a commercial inflection. We’re approaching a decision point that will determine whether it materializes.

"We're approaching a decision point that will determine whether this becomes a commercial inflection — or whether we're building a much larger, better-funded version of the same mission-locked industrial base that has characterized space for sixty years."

We’re seeing the construction of a much larger, better-funded, technologically sophisticated version of the same mission-locked industrial base that has characterized space for sixty years. And the architectural decisions being made right now — under urgency, optimized for sovereignty and defense — will determine whether that assessment is correct.

What The Data Actually Shows

Seraphim's Q4 2025 report is worth reading closely because the details reveal something quite different from the headline.

Where the capital actually went

The three fastest-growing segments year-over-year were Build (+143%), Launch (+117%), and Downlink (+118%). These are all infrastructure and distribution layers — satellites, rockets, ground terminals. Capital is flowing upstream, into the hardware that makes space capabilities possible.

Meanwhile, the segments that declined were Analyze (-33%) and Platforms (-33%). These are the layers where commercial value gets created from space-based data and where end-use markets actually form. The number of deals in the Analyze segment fell by roughly 50%, and no deal in that category exceeded $100 million in 2025.

This pattern is rational given today’s incentives, but it is the opposite of what we would expect if commercial markets were already pulling demand. If true demand were pulling capital into space, you'd see growth in the layers closest to paying customers, including analytics, applications, and productized services. Instead, capital is concentrating in the most capital-intensive, longest-cycle infrastructure layers, betting that demand will emerge once capabilities are deployed.

The top deals tell an even clearer story

Of the top 10 transactions in Q4 2025, seven are either explicitly defense-focused or sovereign capability plays with government anchor customers:

- Stoke Space ($510M), Castelion ($350M), Space Pioneer ($350M): All three largest deals were in Launch, and all three are positioned to serve government missions, with Stoke and Castelion explicitly positioned as Golden Dome beneficiaries.

- Forterra ($188M), ICEYE ($175M), HawkEye 360 ($150M): Defense-focused ISR and communications capabilities.

- Vast ($150M): Speculative beyond-earth infrastructure with no validated commercial demand.

Only K2 Space ($250M) shows clear evidence of designing for productization and repeatability rather than mission optimization — and even K2's valuation is anchored primarily by $500M in signed government contracts.

Even the report's own framing is mission-centric

Seraphim's "What You Need to Know" section identifies six key developments driving the quarter. Every single one is mission-driven or capability-focused:

- First Golden Dome awards (defense mission)

- NASA leadership and U.S. Space Directive (government mission)

- Europe consolidating space industry (defensive industrial policy)

- Blue Origin successful landing (capability milestone)

- SpaceX IPO planning (capability/infrastructure)

- M&A activity (vertical integration for defense contracts)

Not one item describes commercial customers validating demand, pricing power in competitive markets, or space-sustaining revenue growth at scale.

Geographic drivers are all geopolitical

The report explicitly attributes regional growth to sovereign and defense imperatives:

- U.S. investment grew 130% "thanks to enthusiasm for flagship programmes including the Golden Dome"

- Europe's 25% growth driven by "focus on resilience and increased defence spending"

- China deploying capital to build domestic launch and constellation capabilities

This is not market pull — at least not yet in any sustained sense. It is mission urgency doing exactly what missions tend to do.

Of the top 10 deals in Q4 2025, seven are either explicitly defense-focused or sovereign capability plays with government anchor customers. This isn't market pull. It's mission urgency.

None of this implies that investors, companies, or governments are behaving irrationally. In fact, the opposite is true. The risk emerges precisely because rational responses are aligning in ways that historically produce mission-locked outcomes.

Three Forces Converging to Entrench Mission Logic

The same factors that have driven 2025's record investment are also creating structural conditions that make mission-locked architectures more likely, not less:

1. Urgency Suppresses Productization

Geopolitical competition is real. The U.S. Space Force is moving quickly to field proliferated LEO architectures for missile tracking and defense. Golden Dome contracts are being awarded now, with initial phases funded and full-scale deployment timelines measured in years, not decades. Europe is racing to deploy sovereign capabilities after decades of fragmentation. China is scaling domestic launch and constellations aggressively.

Urgency suppresses productization. When a large anchor customer is waiting, the rational choice is to optimize for that customer and defer standardization. The problem: "we'll productize" later' is historically rare.

This urgency produces a predictable outcome: build to the mission, optimize for the first customer, get capability fielded fast.

Productization — the process of designing systems for repeatability, bounded configuration, and multi-customer use — takes time, introduces constraints, and requires accepting near-term compromises in performance or customization. When urgency is high and a large anchor customer is waiting, the rational choice is to optimize for that customer and defer standardization.

The problem is that "we'll productize later" is historically uncommon once systems are fielded and incentives shift. Once a system is fielded and working, the incentive structure shifts toward sustaining and replicating what already exists rather than re-architecting for markets that remain speculative.

2. Defense and Sovereignty Requirements Drive Architecture

The systems being funded in 2025 are explicitly designed to serve national security missions. That's not a criticism — these are legitimate, strategically essential requirements. But it does shape architectural choices in ways that often foreclose commercial optionality:

- Security and classification requirements that preclude co-location, shared infrastructure, or multi-tenancy

- Orbital configurations optimized for specific defense missions rather than commercial service delivery

- Vendor lock and vertical integration driven by supply chain security rather than competitive dynamics

- Bespoke payload integration rather than standardized interfaces

These decisions are rational for the mission. They also make it structurally harder for a second customer — especially a commercial one — to participate without forcing a redesign.

3. Capital Abundance Removes The Forcing Function

SpaceX succeeded in part because capital was constrained during its early years. Elon Musk committed personal capital, but even with that, the company faced real execution risk and limited margin for error. That constraint forced architectural discipline: design for repeatability, because you can't afford to re-engineer every time. Build for reuse, because you need the economics to work at scale.

In 2025, capital is abundant — at least for companies with government anchors. Golden Dome alone could ultimately represent tens of billions in contract value. European defense budgets are expanding. China is underwriting domestic capabilities regardless of near-term economics.

When capital is plentiful and anchor customers are secured, the forcing function that drives productization disappears. Companies can build bespoke systems at scale, absorb high unit costs, and sustain operations through government contracts indefinitely — without ever needing to serve competitive commercial markets.

What Investment Patterns Reveal About Market Formation

Taken together, these dynamics shape not just how capital is deployed, but what kinds of markets—if any—are being allowed to form. The Seraphim data, read through a missions-versus-markets lens, suggests that markets are not forming in proportion to the capital being deployed.

Apply the revenue-responsibility test: follow the money upstream. Where are the paying customers for the Build, Launch, and Downlink investments that drove 2025's growth?

Answer: Predominantly government missions — Golden Dome, sovereign constellations, NASA programs, defense ISR.

Not: Validated commercial demand in space-sustaining markets.

The sectors that actually serve commercial end-users — Analyze, Products — are shrinking both in deal count and capital deployed. This implies that infrastructure is being built ahead of validated demand, based on the assumption that government missions will enable commercial markets to follow.

That assumption may prove correct. But it's an assumption, not evidence of market formation.

Compare this to how GPS created markets

GPS was mission-funded and government-operated. But critical structural decisions preserved optionality:

- Open signal specification allowed commercial receiver development

- Unencrypted civilian signals (even if initially degraded)

- Published interface standards

- Subsequent modernization explicitly designed for non-military users

None of these decisions were required to fulfill the defense mission. In fact, each introduced perceived risk or complexity. But collectively, they transformed GPS from a closed capability into enabling infrastructure that $1+ trillion in commercial activity now depends on.

The 2025 investment wave, by contrast, is concentrating in systems designed first and foremost for government missions, with commercial participation assumed to follow — but not yet designed in.

The K2 Exception Proves The Rule

K2 Space's $250M Series C is the only top-ten deal that clearly demonstrates an intent to productize a historically mission-specific capability class.

K2 is building large, high-power satellite buses — traditionally the domain of bespoke, exquisitely engineered, government-grade platforms. What distinguishes K2's approach is the explicit attempt to create a repeatable platform despite working in a high-performance segment:

- Multi-orbit capability (LEO, MEO, GEO)

- Bounded configuration rather than full bespoke

- Blended customer base (commercial and government)

- Vertical integration for cost and speed, not just security

This is a productization strategy: building systems designed to be copied and configured within bounds, rather than redesigned for each customer.

But even K2 anchors its business case on $500M in signed contracts, the majority of which are almost certainly government. The company is attempting to use mission demand as a bridge to commercial markets — exactly the pattern I described in the SpaceX essay.

K2 may succeed. But the fact that it's the exception among top 2025 deals is telling. Most capital is flowing to companies that are either explicitly mission-locked (defense ISR, sovereign constellations) or building speculative infrastructure without clear paths to commercial validation (beyond-earth plays, logistics platforms ahead of demand).

What We're Actually Building

Step back and look at what $12.4 billion in 2025 private investment is actually funding:

- Sovereign launch capabilities: Stoke, Castelion, Space Pioneer, and others are building domestic launch capacity optimized for government missions and supply chain security.

- Defense ISR and communications: ICEYE, HawkEye 360, Forterra, and dozens of others are building sensing and connectivity capabilities explicitly for national security customers.

- Vertical integration for mission assurance: The Firefly/SciTec and Intuitive Machines/Lanteris acquisitions signal consolidation toward vertically integrated platforms serving defense and civil government programs.

- Speculative in-space infrastructure: Vast, Redwire, and others are building beyond-earth capabilities — stations, logistics, servicing — ahead of validated demand, betting that missions will justify deployment and markets will eventually materialize.

All of this is impressive. Some of it is strategically essential. But it is structurally different from the infrastructure that enabled previous technology revolutions:

- GPS: Open architecture, public signals, standardized interfaces → enabled commercial markets

- The Internet: Open protocols, competitive layers, interoperability requirements → enabled commercial markets

- Commercial aviation: Certified platforms, competitive services, regulatory frameworks enabling multi-party participation → enabled commercial markets

The question is whether the systems being funded in 2025 are being designed with that same optionality, or whether they're being optimized exclusively for their anchor missions.

The Architectural Decisions That Matter

Markets don't emerge simply because capabilities exist. They emerge when systems are designed to accommodate multiple payers, competitive participation, and uses beyond the original mission.

For space-based data centers (which I analyzed in a previous piece), for satellite constellations, for launch platforms, and for in-space services, the decisions that preserve or foreclose market optionality include:

- Security and access models: Can the architecture support multi-tenancy, or does security require single-customer exclusivity?

- Interface standardization: Can payloads, services, or data integrate through published standards, or does everything require bespoke integration?

- Pricing and procurement structures: Are services sold on performance (compute-hours delivered, imagery resolution, bandwidth), or are systems procured as assets for exclusive use?

- Modularity and configuration: Can platforms serve multiple missions through bounded configuration, or does each deployment require fundamental redesign?

- Operational sovereignty: Do architectures enable shared infrastructure with logical separation, or do they require physical separation for each sovereign customer?

These decisions are being made right now, in 2025, as capital deploys and architectures solidify. And they're being made under conditions that favor mission optimization:

- Urgency is high (geopolitical competition)

- Anchor customers are secured (government contracts)

- Capital is abundant (removing discipline)

- Requirements are defense-driven (security over flexibility)

Historically, that combination has been sufficient to harden architectures long before markets have a chance to form.

The point of this analysis is not to argue against mission-driven investment, but to clarify what it takes to convert mission urgency into durable market foundations.

The $12.4 Billion Question

Record investment proves space capabilities will be built. Geopolitical urgency and national security imperatives ensure it. The technology is real, the capital is committed, and the systems will be deployed.

Record investment proves space capabilities will be built. The real question is: are we building for markets or just better-funded missions?

The real question — the one that determines whether this investment wave creates a self-sustaining space economy or just a much larger mission-dependent industrial base — is this:

Are we using mission urgency to fund infrastructure designed with the optionality, standardization, and competitive access that enable market formation?

Or are we optimizing exclusively for sovereign and defense missions, building bespoke architectures at scale, and assuming commercial markets will somehow emerge later from systems that were never designed for them?

History offers a clear lesson: GPS created trillion-dollar markets because it was designed with openness and optionality that weren't required by the original mission. Apollo, the Space Shuttle, and Iridium 1.0 demonstrated extraordinary capability but never escaped their mission contexts, remaining impressive but economically fragile.

What remains unresolved is whether those systems are being designed to evolve beyond their first missions — or whether we are quietly locking in a much larger, more capable version of the mission-dependent space sector we already know.

What makes this moment different from past cycles is not intent, but timing. Architectures are still being shaped, launch is no longer the bottleneck, and commercial demand signals — while not yet dominant — are now visible. That creates a narrow window where mission-funded buildout can still be structured to support markets, rather than foreclose them.

The question, then, is not whether this investment wave should happen. It already is. The question is how to ensure it becomes a foundation for markets rather than a ceiling that constrains them.

Turning Mission Urgency into Market Foundations

If the goal is to ensure that today’s mission-driven buildout compounds into durable markets rather than hardening into permanent dependency, the encouraging news is that this outcome is still tractable. That responsibility is shared across investors, companies, and policymakers.

What Investors Can Do

Investors are uniquely positioned to reward optionality, not just capability.

- Underwrite second customers early. Defense revenue is a strong anchor, but insist on a credible path to diversified demand — specific use cases, pricing units, and buyers beyond the first mission sponsor.

- Fund repeatability milestones, not just delivery. Tie capital to indicators like standardized interfaces, integration time, unit cost reduction, and configuration reuse.

- Prefer bounded platforms over bespoke excellence. Companies that say “no” to one-off requirements are often preserving more long-term value than those that maximize near-term contract scope.

Why care? Because defense can be a great business — but it’s a low ceiling for long-term market formation. Markets reward optionality with higher multiples, broader exits, and resilience across political cycles.

What Companies Can Do

Operators control the architectural choices that determine whether markets can ever emerge.

- Design dual-lane architectures. Separate mission-specific security or payload requirements from a commercializable core product.

- Standardize interfaces early. The first major customer often becomes the architecture — intentionally or not.

- Price like a service even when procured as an asset. Market formation follows units, not platforms.

What Policymakers Can Do

Governments already recognize the need for procurement reform — but execution matters.

- Buy services — and then resist the understandable urge to customize them in ways that quietly turn services back into bespoke programs. “As-a-service” procurement only preserves optionality if buyers avoid layering bespoke requirements that quietly re-missionize the offering.

- Reward interoperability and shared infrastructure. Standards bodies, common testbeds, and open interfaces enable competition and cost curves that missions alone cannot sustain.

- Treat market spillover as a security objective. Resilient, competitive ecosystems ultimately strengthen national capability more than exquisite, single-purpose systems.

The goal isn’t to weaken missions. It’s to ensure mission-funded buildout becomes a floor for market growth so that today’s urgency compounds into a space economy that can ultimately sustain itself.

Five years from now, the difference will not show up in mission performance—it will show up in who your customers are allowed to be.

For operators, this isn’t an abstract industry debate. The architectural decisions being made now will determine whether today’s programs become platforms that compound or systems that must be continually re-justified to a single sponsor. Five years from now, the difference will not show up in mission performance — it will show up in who your customers are allowed to be.