The long-term viability of the space economy hinges on a simple but often overlooked truth: we will not see a resilient, high-growth commercial space sector until Space-Native markets mature.

“Government demand sustains the space industry, but it cannot scale it.”

Government-backed national security programs and scientific missions have underwritten the space sector for decades, and they remain the backbone of the industry today. But, although essential, government demand is structurally capped. While it sustains the industry, it cannot scale it. Even worse: the dominance of government as the primary driver of space expenditures leaves the industry exposed to political cycles, budget rescissions, procurement delays, and shifting strategic priorities. It also means valuations are distorted: most revenue today ultimately traces back to government funding rather than private-sector demand.

“A resilient space economy requires revenue that flows from real commercial demand — not budget cycles.”

If we want a self-sustaining commercial space economy, we need markets where user fees — whether from commercial or government buyers — directly fund the space infrastructure or distribution layers that deliver capabilities from orbit. That’s where the distinction between Space-Native and Space-Enabled markets becomes indispensable.

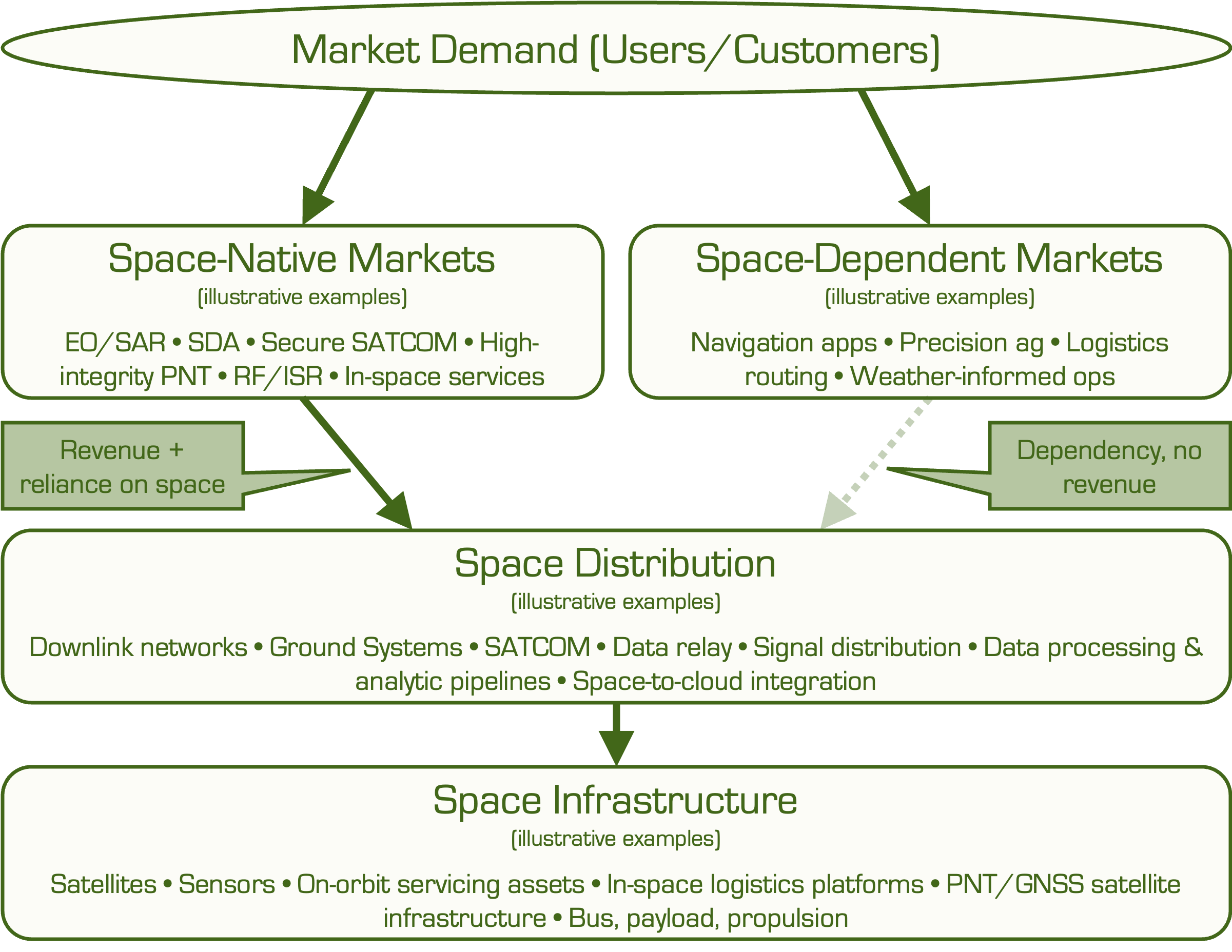

Space-Native vs. Space-Enabled: A Lens for Commercial Reality

The conventional narrative around the “$570 billion space economy” blends two fundamentally different categories of demand:

Space-Native markets

Markets where users, whether government or commercial, rely on and pay for space-based capabilities. User fees flow upstream into the companies that operate satellites, build sensors, deliver space-derived data, or maintain on-orbit services.

These are the only markets that generate monetizable demand for space companies and the only source of long-term, scalable growth.

Space-Enabled markets

Markets that rely on space-based signals or data but pay nothing for the underlying assets. They depend on free public infrastructure such as:

- GPS/GNSS

- AIS

- NOAA and EUMETSAT weather satellites

- Landsat, MODIS, GRACE, Sentinel-1/Sentinel-2

- (soon) NISAR

Space-Enabled markets create enormous economic value, but none of their revenue flows to the space sector. They are part of the impact of space, not the economy that funds it. Understanding this distinction is essential for investors, founders, and analysts evaluating real business opportunities in the space sector.

“Space-Enabled markets measure the economic impact of space, not the commercial viability of space companies.”

What Actually Makes a Market Space-Native? Follow the Revenue.

A market is Space-Native if:

- Its core product or service fundamentally depends on capabilities delivered from orbit, and

- User fees or product revenue flow to the companies that operate or maintain those space-based capabilities.

If a market relies on space but no one pays the space infrastructure providers, it is Space-Enabled. Space may be critical to the market, but the market is not, in turn, funding the capability — no matter how critical the space dependency appears.

A few examples illustrate the point:

- Agricultural firms using free Sentinel-1 SAR or free GPS for crop monitoring and automated guidance → Space-Enabled

- Logistics platforms using free GPS or free AIS for routing and vessel tracking → Space-Enabled

- Weather-dependent utilities or airlines using free NOAA and EUMETSAT data → Space-Enabled

"The industry cannot scale until we separate demand that actually pays for space from demand that only benefits from it.”

By contrast:

- Insurers purchasing commercial SAR for loss assessment → Space-Native

- Defense customers buying RF geolocation/signals intelligence (SIGINT) or high-fidelity EO intelligence → Space-Native

- Commercial firms paying for resilient PNT alternatives → Space-Native

The definition has nothing to do with whether the buyer is commercial or government. It’s about whether revenue flows into orbit. The test is simple: If user fees sustain the infrastructure that makes the capability possible, the market is Space-Native. If they don’t, it’s Space-Enabled.

“If revenue never reaches the companies operating or maintaining space assets, the market isn’t Space-Native — no matter how dependent it appears.”

Global Spending: Understanding What the Numbers Really Mean

The global space economy is commonly quoted at ~$570 billion (Space Foundation, 2023), with roughly 78% described as “commercial.” But most of that 78% represents Space-Enabled downstream activity — economic value created using space infrastructure, not revenue paid to space infrastructure providers.

Most of the “commercial” number is Space-Enabled downstream activity.

Ride-hailing services, delivery apps, navigation, weather services, logistics optimization — almost none of these revenue streams flow back to the companies operating satellites, buying launch services, or managing space asset distribution.

The revenue that does reach orbit comes primarily from governments.

NovaSpace’s Government Space Programs 2024 Report estimates global public space spending at ~$135 billion, more than half of it defense-related. That number, while smaller, is much closer to the real scale of money that reaches space operators, manufacturers, and in-space service providers.

This distinction matters because:

- Space-Enabled market size is useful for measuring the economic impact of space, but

- It is meaningless for evaluating TAM, business cases, or revenue potential for space companies.

The space sector’s true economic backbone is the Space-Native layer, and today, that layer is still dominated by government demand.

Government’s Dual Role: Catalyst and Constraint

Government’s influence on the space economy is both profound and complex.

1. Government is the primary source of Space-Native demand.

Governments pay for:

- Earth observation

- Climate and weather data

- RF and EO intelligence

- SATCOM

- SDA and defense-related services

- Technology demonstrations and early-stage R&D

These are all true Space-Native markets - the government is the paying customer funding the deployment of the necessary capabilities to support these services.

2. Government simultaneously suppresses commercial formation by providing free alternatives.

Free GNSS, free SAR (Sentinel-1), free weather data, free climate datasets — all of these enable massive Space-Enabled markets without stimulating commercial demand for paid alternatives. This dual role is not a contradiction — it is the structural reality of today’s space economy. Indeed, many of these services might simply not exist until the economics of space infrastructure become substantially more attractive.

But, as an outcome of this arrangement, government action that works to sustain the Space-Native layer simultaneously crowds out the commercial potential and market-driven innovation of that layer as it offers "free" alternatives to market-based solutions. For instance, commercial SAR providers must compete with Sentinel-1's free, globally available data, making it harder to justify premium pricing even for higher-resolution or more timely products.

The Core Insight: Growth Depends on Expanding Commercial Space-Native Markets

Government demand for orbital capabilities is essential, and it will remain essential. But it cannot be the long-term engine of growth for a self-sustaining space economy. Despite driving the near-term growth of the space sector, these budgets are ultimately capped. In the absence of external threats or geopolitical competition, these budgets generally increase slowly, shift with political cycles, and cannot scale exponentially. Sustained growth in the space economy ultimately depends on commercial customers paying directly for capabilities delivered from orbit — capabilities that:

- Outperform free government alternatives

- Solve urgent commercial problems

- Justify recurring revenue at a meaningful scale

Near-term opportuniities include commercial EO/ISR and secure communications, where government buyers are already procuring commercial alternatives. Mid-term prospects like high-integrity PNT and commercial SDA are emerging as critical national security needs. Longer-term, in-space logistics, manufacturing, and, eventually, tourism and off-earth living represent the ultimate expression of Space-Native demand.

This includes markets such as:

- High-integrity commercial PNT

- Commercial EO/ISR

- Commercial SDA

- Secure commercial communications

- In-space logistics and servicing

- Eventually, in-space manufacturing and resource utilization

- And, longer term, space tourism and off-earth living

These Space-Native markets are the pathways to a space economy that grows based on economic pull, not government appropriations. And the associated market size drives investment as revenues flow upstream from the market to space services providers.

“Until Space-Native markets grow large enough to stand on their own, the commercial space economy will remain exposed and fragile.”

I’ll explore this further in upcoming analyses on market segmentation, associated revenues, and the use cases that define real Space-Native demand.